[ad_1]

All the guilt of the survivors was fleeting for residents with their homes standing after a wildfire ripped apart the Los Angeles area three months ago.

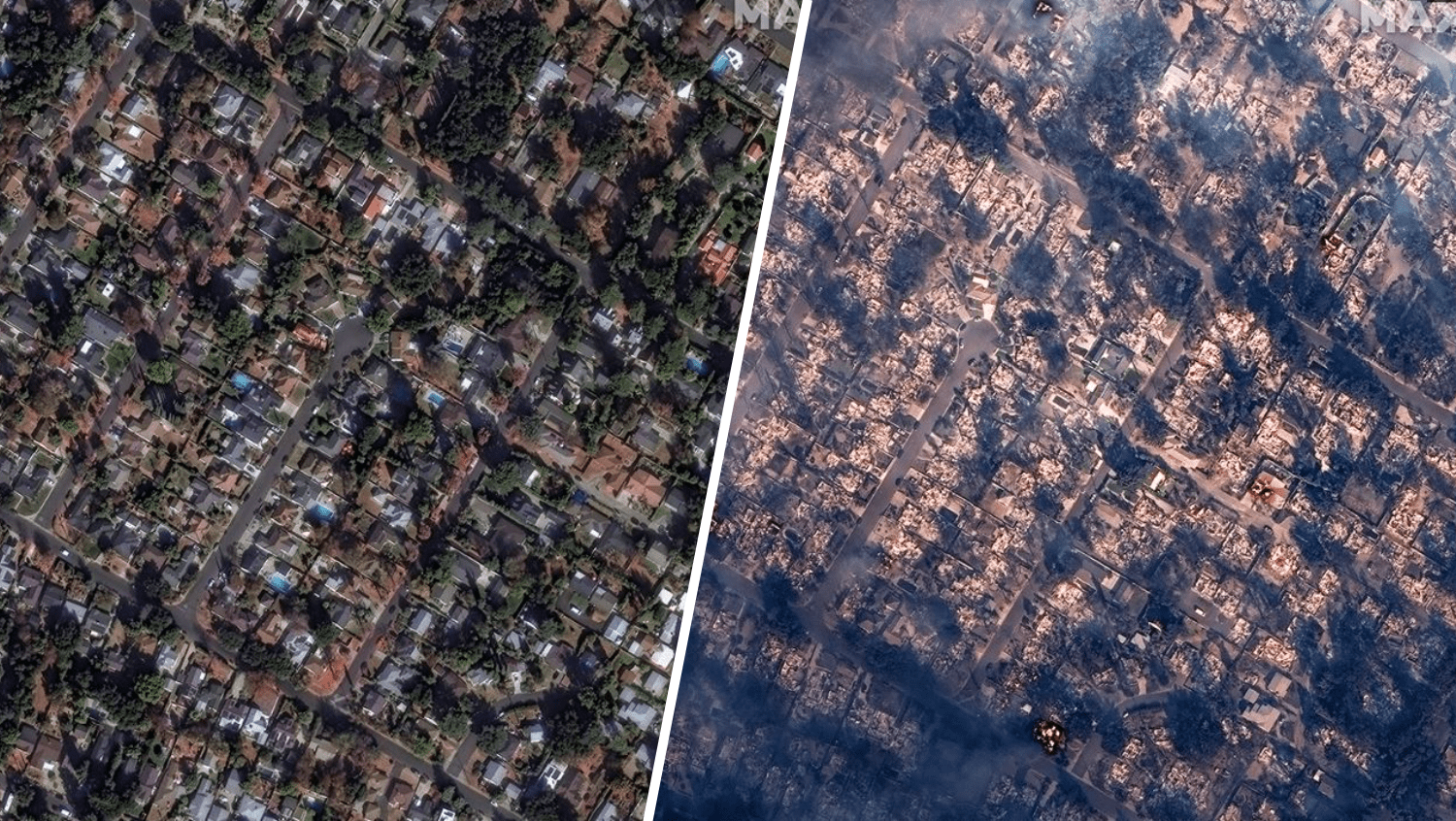

Many were worried that smoke from the Eton wildfire, which destroyed more than 9,000 structures and killed 18 people, brought toxins such as lead, asbestos and heavy metals into the home. However, they struggled to convince the insurance company to test their property and made sure it could return safely.

Data scientist Nicole McCalla said embers burned more than half of her roof, damaged several windows and eaves, leaving her home in Altadena filled with ashes, debris, soot and damaged appliances. She said the insurance adjuster said the USAA would pay for the pollution test, but after choosing a company and returning the results, her claim was rejected. The adjuster said the company will only cover tests in households that have suffered major damage.

“Every item is a fight,” McCalla said. “It’s a denial and pleading, a denial and appeal, and you’ve been waiting for weeks, weeks, weeks.”

Crowdsourcing Pollution Data

Maccalla and others have come together to share indoor environmental test data and edit the results into an online map. According to the group, of the 81 homes tested for leads so far, all exhibit elevated levels.

“I’ve already reached out to several people and said, ‘Thank you for publishing this map… because my insurance company changed my mind and approved the test,” McCalla said.

Many homeowners have personally paid for testing after the insurance company refused, revealing the coverage gap. The group hopes that the data will help residents who cannot afford to persuade insurance companies to cover testing and repairs.

“If I can prove that my community is not suitable for human habitation, I might be able to show that my home is not,” said Jane Lawton Potel, founder of Eton Fire Residences United.

It’s not easy to understand when and when to return home. Fine printing of insurance contracts can be frustrating and confusing, and the government has not stepped in to seek help.

The Federal Emergency Management Agency said there are no plans to conduct extensive environmental testing. The Los Angeles County Department of Public Health tracks environmental testing by only a handful of people, primarily from academic researchers and government agencies, but most studies assess outdoor pollution.

Toxic Air and Limited Coverage

Reports from other urban wildfires show increased levels of heavy metals, including lead and polycyclic aromatic hydrocarbons (PAHs), such as benzene, which burn at incredibly high temperatures, leading to negative health risks. However, insurance companies have not performed standardized testing of these contaminants.

While home insurance covers a wide range of fire damages, there is an increasing number of disputes over what damages must be covered if the flames do not torch your property.

California Insurance Commissioner Ricardo Lara has released a breaking news that will hold businesses accountable to properly investigate reported smoke damage. However, many residents are left to fight for the press anyway.

Janet Lewis, a spokesman for the Insurance Information Institute, which represents many major insurance companies, said it is difficult to compare neighbors because all claims are unique due to the physical structure of each home, actual damages and defined insurance coverage restrictions.

“It varies and insurance companies are sensitive to what the claim is,” Lewis said. “You have to work with your insurance company and be reasonable about what happened.”

Dave Jones, director of the University of California, Berkeley Climate Risk Initiative, said the test should be covered even though some insurers disagree.

“It’s completely reasonable for people to do some kind of environmental test, so make sure their homes are safe and their property is safe,” Jones said. “We’re talking about very devastatingly hot fires where all sorts of ingredients melt and some of them become toxic.”

The state’s plan struggle

The state’s last resort insurance company known as California Fair Access to insurance requirements has been scrutinized for years on how it handles claims of smoke damage. The 2017 change to a fair plan is limited to “permanent physical changes.” This means that smoke damage must be visible or detectable without lab tests for approved claims. State officials said the threshold was too high and illegal and ordered the change.

Dylan Shaffer, the lawyer leading a class action lawsuit challenging fairplan thresholds, said he was surprised that civil airlines are challenging similar fire damage claims.

“The damage is not caused by smoke, the damage is caused by fire,” Schaffer said. “They save them money, so they complicate it.”

Meanwhile, residents of Altadena from Fairplan say their claims are still being rejected. Jones believes that debate only ends when lawmakers take action.

Fairplan spokeswoman Hillary McLean declined to comment on the ongoing lawsuits and individual cases, but said Fairplan would pay all applicable claims based on the Adjuster’s recommendations.

“Our policy, like many others, requires direct physical loss due to coverage,” McLean said.

I’m worried about the safety of my child

Potel said the first inkling that her home could be toxic came after meeting her AAA insurance adjuster the day after the fire. She was wearing a mask, but her chest still aches, her voice squealing, and she wondered if her home was safe for the 11-year-old.

Stephanie Wilcox said her toddler pediatrician recommended that their home be tested. Her farmer insurance contract includes reed and asbestos coverage in addition to her wildfire coverage, but after multiple denials she paid out of pocket.

“After the initial inspection, (farmers) said the restoration would cost around $12,000 and it would be habitable so they could return to tomorrow,” she said. “But now there’s no way.”

She will cite the results to seek new estimates including lead reductions and other costs.

Similarly, Zach Bailey called for a contamination test in late January. The house he shares with his wife and toddler sits on the island of his home, where he saved most of it in the blocks wiped out by the fire. A few months after the denial, the state farm agreed to pay for lead and asbestos testing as the restoration company cited federal workers safety regulations.

That must have been so difficult, he said.

“I feel that insurance companies should have a playbook at this point,” he said. “They should have a process that keeps people safe because this isn’t the first disaster like this.”

[ad_2]Source link